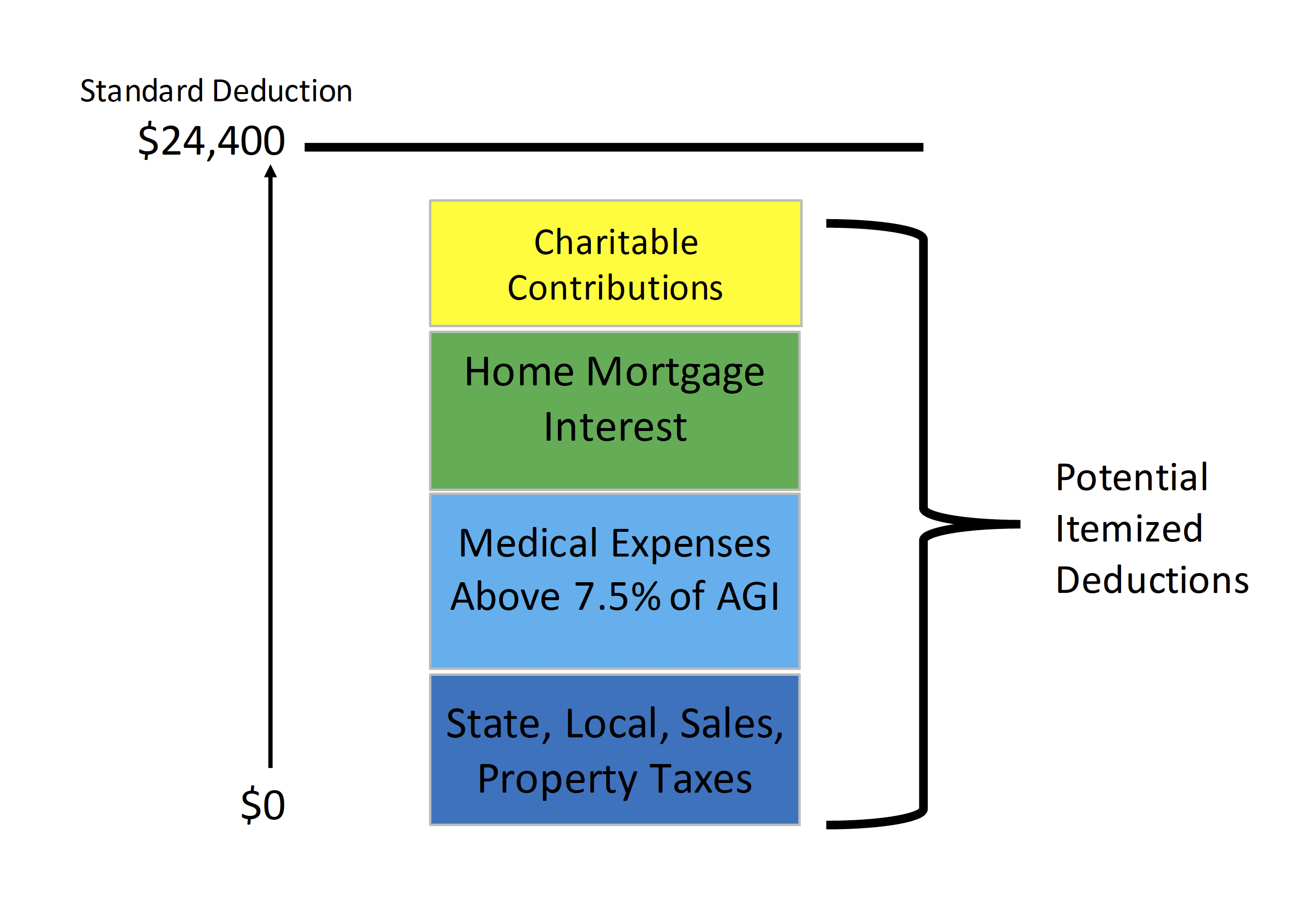

Charitable Contributions Subject To 10 Floor

March 2019 Charitable Contributions Are They Still Tax Deductible Marin Financial Advisors

The Charitable Contributions Deduction Mercatus Center

The Tax Break Down Charitable Deduction Committee For A Responsible Federal Budget

Pin By Morgan Jackson On Procurement And Sponsorship Lake Oconee Charitable Donations Public Service

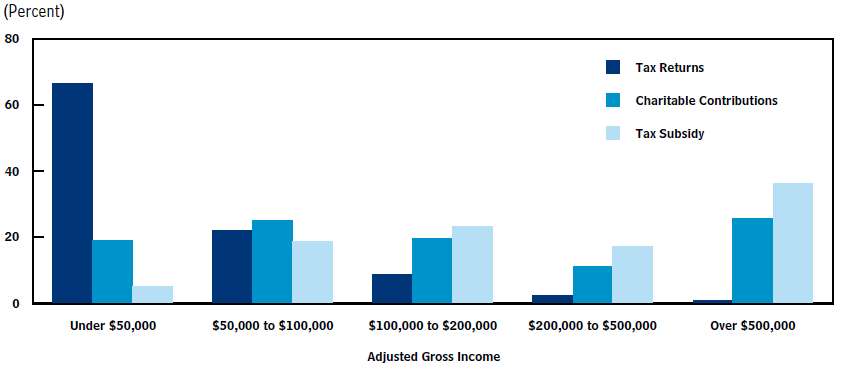

Covid 19 And Charitable Contributions By Individuals And Businesses The Cpa Journal

Https Fas Org Sgp Crs Misc If11022 Pdf

Special rule for california wildfire relief contributions.

Charitable contributions subject to 10 floor.

Pin By Morgan Jackson On Procurement And Sponsorship Lake Oconee Charitable Donations Public Service

Acceptance Package College Acceptance Acceptance College

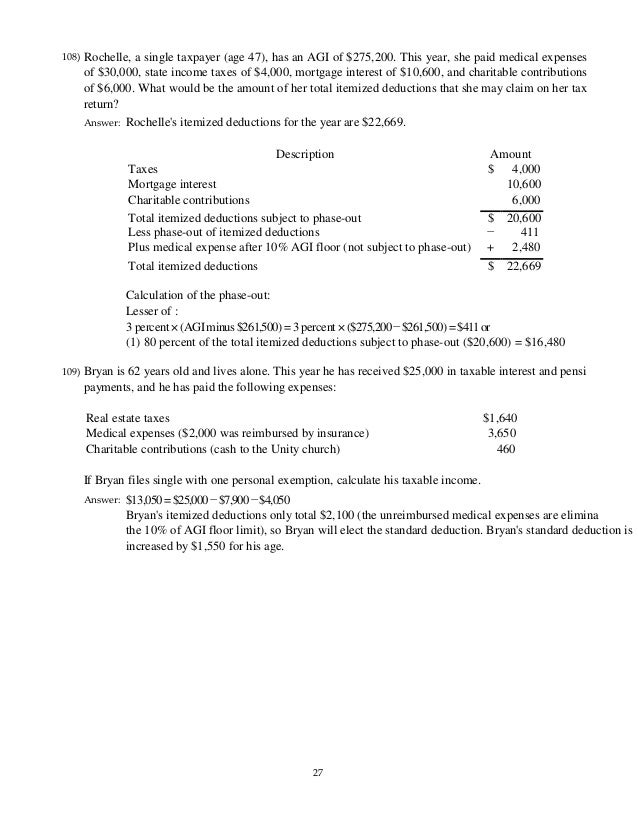

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Wsj Tax Guide 2019 Charitable Donation Deduction Wsj

Source : pinterest.com